now loading...

Continuing my narrative about Europe’s quest to achieve financial autonomy, I wanted to pick up on the dominance of European investment banking by just five US firms and the contradiction it poses. Yes, contradictions. Because at the same time as US IB dominance in Europe represents a strategic vulnerability for Europe in a crisis, in normal times it enables European firms to be more ambitious on the world stage, to achieve larger deal sizes, lock in keener pricing, minimise execution risk while offering access to global markets, including the world’s deepest.

It’s obvious but just in case, we’re talking – in alphabetical order to avoid accusations of bias – Bank of America, Citigroup, Goldman Sachs, J.P. Morgan, and Morgan Stanley, with Jefferies playing a more limited role.

Let’s start with some datapoints to illustrate the status quo. US firms had a market share of more than 50% of European equity capital markets ( ECM ) in 2025, and six US firms occupied the top 10 of LSEG’s league table. In completed M&A with any EMEA involvement, the top five and eight of the top 10 advisers were American. Meanwhile, five of the top 10 European sovereign bond bookrunners were US banks, and they led almost a third of the total funds raised in the syndicated sovereign market. And US banks book-ran over a fifth of the US$565 billion in European corporate bond issuance.

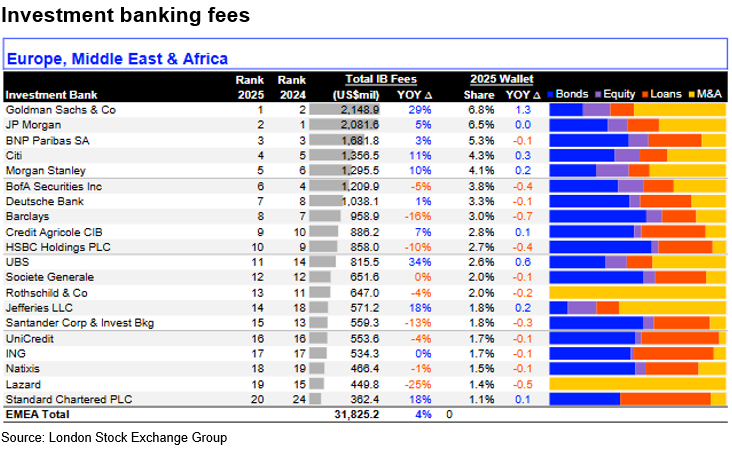

It’s not just about the reflected glory of league-table position. It’s also about how that rolls up into wallet. EMEA investment banking fees increased by 4% in 2025, LSEG data show. But Goldman Sachs increased its fee-take by 29%, Jefferies by 18%, Citigroup by 11%, and Morgan Stanley by 10%.

Contrast that with the European experience: HSBC’s fees fell by 10%, Santander’s by 13%, Barclays’ by 16%. Only UBS spared Europe’s blushes by increasing its fee-take by 34%, clearly putting its absorption of Credit Suisse firmly behind it. All told, US firms earned 28.5% of the US$31.8 billion EMEA IB fee pool and filled five of the top six fee positions.

The US firms’ broad and deep European advisory, capital markets origination, and distribution footprints follow decades of focused endeavour across Europe, aided and abetted by the not-so-secret competitive weapon of a deep home market that gives them an enormous recurring source of know-how and revenue to build off.

It’s hard to see how that changes, even if the EU single capital market evolves in accelerated fashion. The harsh reality for European policymakers and banks is that US firms dominate M&A flows and financial sponsor activity globally, including into and out of Europe. The largest pool of global capital resides in the US and US investors are big end-buyers of European securities. And don’t think for a moment that US banks only distribute into the US. They have deep relationships with the European and Asian buyside, too.

Structural vulnerability

Europe’s reliance on a handful of US firms to intermediate its capital markets and conduct a huge proportion of its advisory assignments creates a structural vulnerability. Having dominant underwriters, advisers, market‑makers, and distributors in Europe regulated and run from the US exposes Europe’s access to capital and deal execution to US monetary policy, regulation, risk appetite, and US economic realities.

The concentration of talent, balance-sheet muscle, and innovation sitting within US banks erodes Europe’s intermediation and advisory capacity, confining most domestic banks to low‑margin lending while US firms set the pace in investment banking.

No competitive win

A few words on corporate lending. Yes, European banks dominate this area. But not because of competitive pushback against any US onslaught, but because US banks just don’t play in that sandpit. They apply their competitive lending muscle to land lead roles on syndicated loan facilities for a nucleus of large European companies, and focus on investment-banking-like areas such as acquisition and leveraged finance, and sponsor‑driven transactions. In short, they skim off the high fee-paying business.

Nor do they clog up their balance sheets with European loan exposure. They treat European lending as a fee‑based investment banking business. Their originate-to-distribute business models drive aggressive sell‑downs. US banks had a 15% share of mandated arranger facilities in 2025, acting on US$176 billion‑equivalent of European syndicated loans. But they likely have no more than 2%-4% of European corporate loan outstandings on their balance sheets.

This contrasts sharply with the long‑term, relationship‑driven obligations of European banks, which have deep bilateral and syndicated loan exposure, provide committed lines of credit and working capital facilities amid a broad suite of corporate‑banking services that drive cross-sell into FX, cash management, trade finance, and other products. And no, corporate banking cross-sell does not lead to plum investment banking assignments, despite the narrative that is constantly spun.

Constraints and risk appetite

Europe’s inability to build globally competitive investment‑banking franchises is partly the product of structural constraints ( a fragmented fee pool and lack of a single capital market ), partly due to their failure to break into the US domestic market that’s killed their global ambitions, and partly due to their more constrained risk appetite.

Europe’s heavy reliance on bank lending depresses IB capacity and fee volumes and limits the opportunities for European banks to build the kind of high‑intensity underwriting and distribution engines that thrive on rapid capital turnover. Post‑crisis reforms, meanwhile, have constrained European banks’ ability to deploy balance sheet into underwriting and risk warehousing.

Europeans have no choice but to operate within Europe’s structural limits, but those constraints don’t bind US banks operating in Europe simply because they don’t depend on Europe’s fragmented fee pools or slower capital‑markets dynamics. US banks plug Europe into their own far larger, faster, and more liquid global platforms. US banks in Europe draw on the scale, earnings power, investor demand, and capital‑recycling capacity of US and global markets. Their European operations are satellites of a much larger machine.

So where does all the above leave Europe? On the plus side, US banks massively boost Europe’s underwriting capacity, and that shapes pricing and liquidity for the better. They enable larger deal sizes, reduce execution risk, raise risk appetite and offer global reach.

On the downside, Europe’s dependence on US firms becomes acute in a crisis, as that would mean the firms controlling Europe’s capital‑raising channels, access to liquidity and advice operate outside the ambit of European policymakers and play to whatever tune is being struck up in Washington.