now loading...

Investors continue to be selective and focus on strategies with downside protection in the form of modest leverage or asset backing that provide access to companies and assets somewhat insulated from global trade tensions.

In this environment, both private credit and insurance-linked securities ( ILS ) are emerging as particularly attractive opportunities, offering differentiated return profiles under mounting macroeconomic uncertainty. These strategies are able to bring diversification through reduced correlation with listed markets and exposure to distinct sources of risk.

“The more intense the volatility that we see, and the more disrupted the liquidity is in regulated channels, such as banks and insurers,” says Nils Rode, Schroders Capital’s chief investment officer, “the more opportunities we will see in private credit, in particular.”

As traditional lenders continue to retrench under the weight of regulatory capital requirements and balance sheet pressures, private credit funds are stepping in to fill the void, offering tailored financing solutions across sectors that banks can no longer serve efficiently. This structural shift in capital provision is creating long-term opportunities for private lenders with flexible mandates.

For those hunting for diverse and stable income, infrastructure debt looks appealing in today’s uncertain environment. Backed by essential services, such as transportation, energy transition and digital infrastructure, these assets often enjoy contracted cash flows and inflation-linked returns.

Infrastructure debt also benefits from strong downside protection due to its senior secured position in the capital structure, making it increasingly attractive to pension funds and insurers seeking to match long-dated liabilities with low-volatility assets.

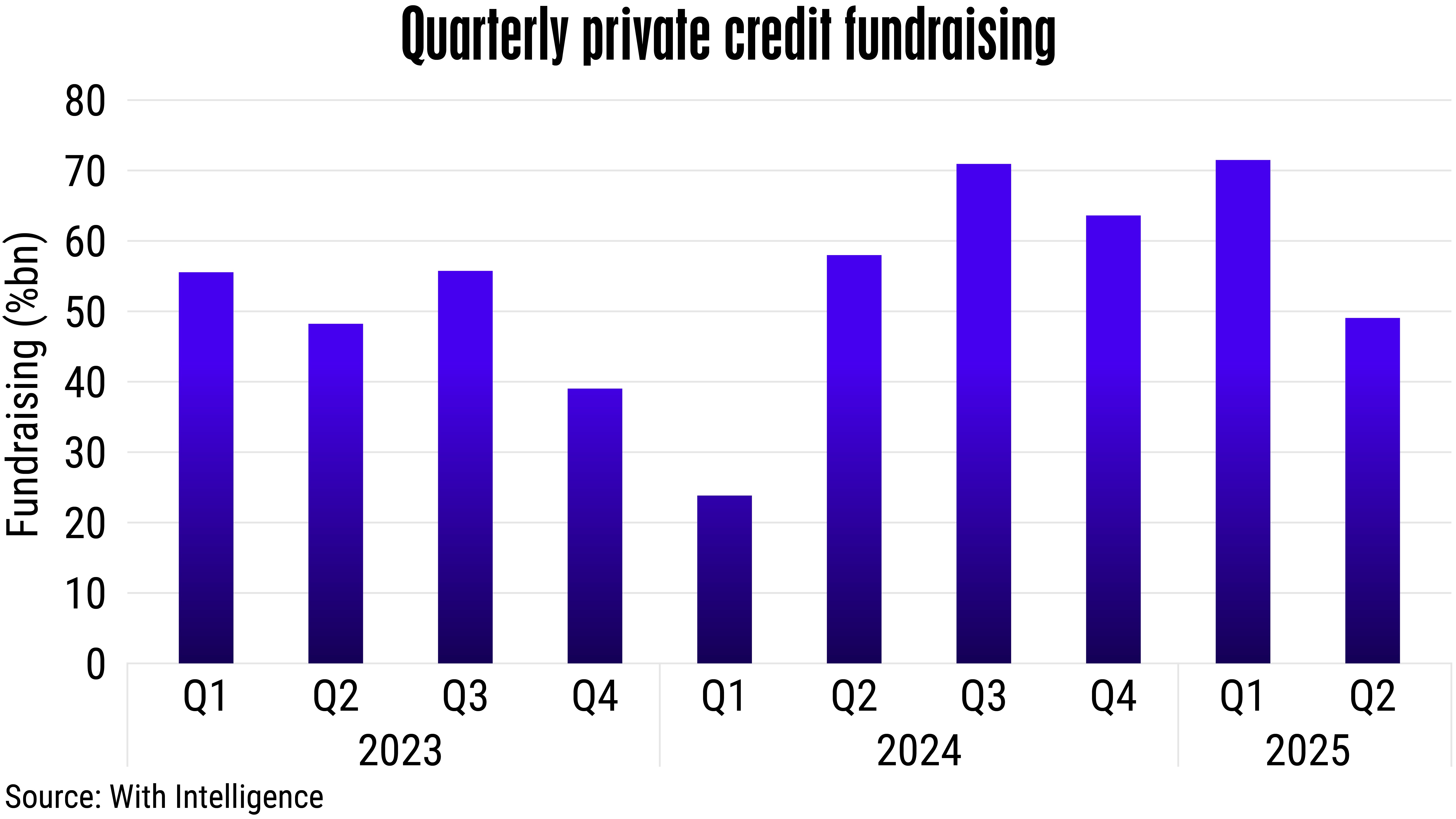

Global private credit fundraising in H1 2025 totalled US$124 billion, according to UK-based data provider With Intelligence, putting the asset class on pace to surpass 2024’s full-year total. Direct lending continues to dominate the fundraising landscape, but investor appetite is clearly evolving.

Over 50% of new fund launches now focus on opportunistic credit and specialty finance strategies, as investors diversify exposure amid lingering interest rate pressures, geopolitical instability and tariff-related volatility. This shift reflects a growing demand for strategies that can dynamically respond to dislocations in both public and private markets.

ILS also continue to stand out for their lack of correlation with the macroeconomy, providing a much-needed respite from unstable markets. Unlike traditional credit or equity investments, ILS instruments are driven by insurance event outcomes – such as natural catastrophes – rather than interest rates or corporate earnings.

This structural independence from economic cycles offers valuable portfolio diversification. In addition, ILS often offer attractive risk-adjusted returns in a yield-starved world, particularly when catastrophe activity remains below expectations.

The capacity of the ILS segment reached a record US$107 billion at the end of 2024, according to a report by AM Best and Guy Carpenter, driven by retained earnings and fresh capital inflows. This growth was supported by two consecutive years without significant catastrophe losses, which allowed investors to enjoy strong returns while reinvesting gains.

Catastrophe bonds, in particular, recorded the most expansion, benefiting from heightened investor demand and improved pricing dynamics. By the end of 2024, capacity in the 144A natural catastrophe bond market surpassed US$45 billion, highlighting renewed confidence in the asset class.

Property catastrophe capacity, in January 2025, exceeded demand for the first time in several years, leading to overall risk-adjusted rate decreases. The Guy Carpenter Global Property Catastrophe Rate on Line Index fell by 6.6%, marking a reversal from the nearly 30% increase seen two years earlier when supply was scarce and demand surged following major loss events.

The retrocession market also experienced a softening trend, with capacity widely available after another loss-free year. Rates in the retro market declined by 10% to 20%, reflecting improved investor sentiment, strong capital inflows and a more stable risk environment across the reinsurance value chain.